Agent-ready lending is the practice of preparing a lender's own digital surface so that AI agents can reach it directly, conforming to open agentic-commerce standards, rather than routing customers through a single commercial aggregator. It matters because AI assistants are becoming a real demand surface for credit, and in a regulated category visibility is earned through native reachability rather than bought. The durable position is to be the destination an agent transacts with, not inventory ranked inside another company's marketplace.

This is a category point of view, not a pitch. The Law-to-Code Methodology treats governance as architecture rather than as text; the same discipline that decides where AI investment compounds (the Architectural AI pillar) and what happens when agentic procurement goes wrong (the Agentic Procurement Failure pillar) applies, at the product layer, to a lender's own reachable surface. NETEVO's principal is a registered Trans-Tasman patent attorney and systems architect.

What is agent-ready lending? #

Agent-ready lending sits inside the broader shift to agentic commerce, in which AI agents discover, compare, and transact on a person's behalf. To be reachable, a lender exposes its capabilities through open, multi-vendor standards rather than a single proprietary integration. These standards are un-owned by any single lender or aggregator: the Model Context Protocol (MCP), an open-source standard for connecting AI applications to tools and data; the Agent-to-Agent protocol (A2A), an open standard for interoperability between agents built by different vendors; the Agent Payments Protocol (AP2), an open protocol for agent-initiated payments; and the Agentic Commerce Protocol (ACP), an open standard for commerce between buyers, their AI agents, and businesses. Several now sit with neutral standards bodies — MCP and A2A under the Linux Foundation, AP2 under the FIDO Alliance — which is the governance signal that a standard is genuinely un-owned, not merely openly licensed. Conforming to these on its own surface makes a lender addressable by agents without ceding the customer relationship.

The word that matters is "surface": an exposed, agent-reachable capability the lender owns and operates.

Why can lenders not simply buy their way onto AI assistants? #

In most commerce, a brand without organic visibility can buy placement. In regulated lending that route is not reliably open: advertising on AI assistants is nascent, and credit is among the most constrained categories anywhere. Assume paid placement will not carry you, so visibility is earned through direct, native reachability. Owning your surface is not one option among several; it is the only dependable route in. A lender that waits to be listed has already conceded the surface.

Why this is no longer hypothetical (updated 17 June 2026). The "lenders as inventory" moment has now appeared in a live product. In its ChatGPT personal-finance experience — launched around 15 May 2026, with account connections via Plaid across roughly 12,000 institutions and analysis by GPT-5.5 Thinking — OpenAI has confirmed a forthcoming Intuit partnership that surfaces credit-card recommendations with approval odds, alongside tax-impact analysis, inside the assistant. That is exactly the pattern this piece describes: lenders ranked as supply an agent presents to a consumer, rather than destinations the consumer reaches directly. The point for an Australian or New Zealand audience is not that this is live here — it is United States-only today, available first on ChatGPT Pro and then Plus, and should not be read as available in the ANZ market. Treat it as a leading indicator and prepare your own surface before the same pattern arrives locally.

How do you conform to open standards without surrendering control? #

The goal is sovereignty and interoperability together, not a trade-off. A lender conforms to the open protocol, implements it on its own surface, and keeps the regulated relationship on its own licence. This is the pattern neutral interoperability standards take in other regulated industries. In health-data exchange, the standard is openly published and neutral, and each participant implements it within its own systems rather than routing people through one central operator. The standard creates interoperability. It does not create a landlord.

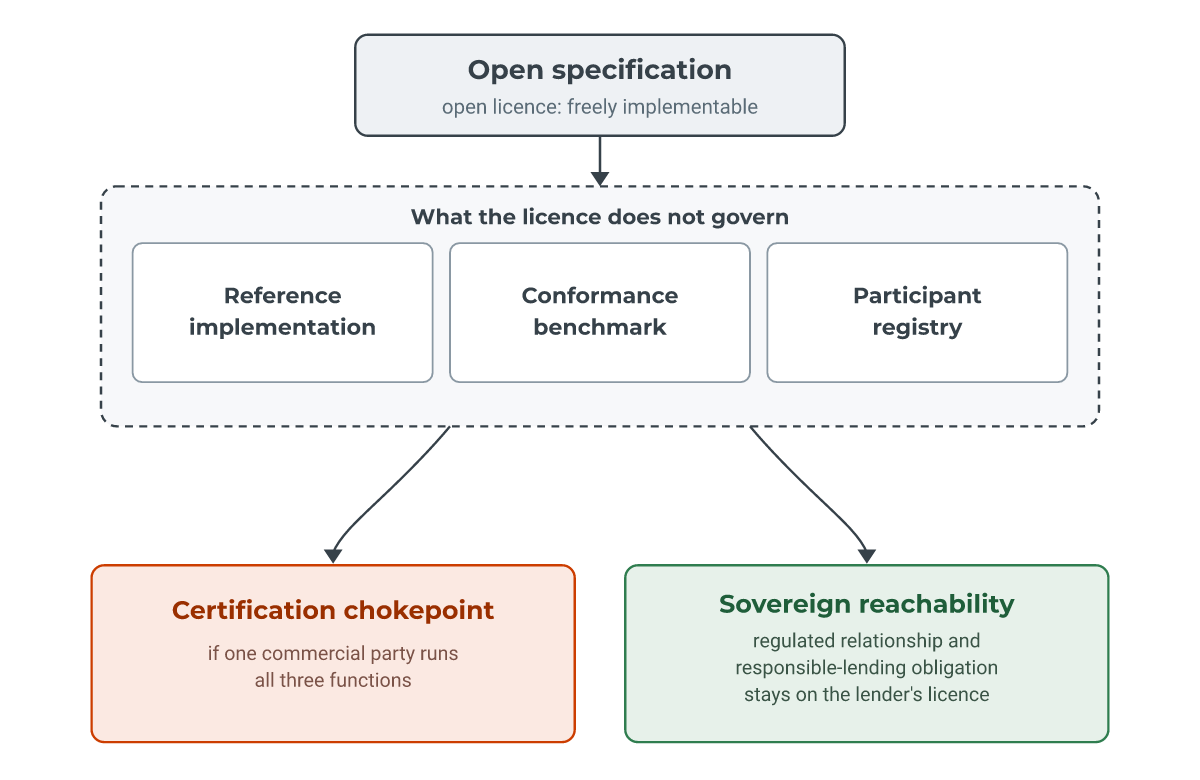

Why is an open licence not the same as a neutral operator? #

This is the distinction that decides the outcome, and it is easy to miss. An open licence governs a document: it tells you the specification is freely available and freely implementable. It says nothing about who runs the reference implementation, the conformance benchmark, and the participant registry. Those three functions are where power actually sits. If a single commercial party operates them, and especially if that party also operates a competing marketplace, the openness of the licence is a veneer over a certification chokepoint. An open licence is not a neutral operator. Certification should be measured against a neutral standard, not against one operator's instance of it.

What should a lender watch for when an aggregator invites it into an agentic-credit pilot? #

Treat an invitation into a pilot as a commercial negotiation, not a technical favour. The signals are consistent:

- Governance, not just licence. Ask who runs the reference implementation, the benchmark, and the registry. An open licence does not answer that.

- "Help shape the benchmark." That can mean feeding your pricing, decisioning, and conversion behaviour into a competitor's back-office and benchmark, which then ranks you.

- Legitimacy by participation. Joining legitimises the registry you will be measured by, and raises switching costs across the industry.

- Certification as a leash. Whoever certifies can tier, re-cut, or withdraw the badge. Certify against a neutral standard, not one operator's instance.

- The role you are cast in. If every worked example makes you a passive endpoint, the pilot is casting you as supply.

- Where the record accrues. During a pilot, the audit trail and case history build up on the operator's side. Switching later means unwinding that dependency and leaving your regulated record in another company's system.

- Who holds the duty. These protocols are jurisdiction-neutral and transfer no compliance burden. Clarify, gate by gate, who holds the obligation, the disclosure, and the audit trail.

- Silence on commercial terms. The marketplace endgame is to aggregate demand, then tax supply. Silence on the take-rate is the tell.

Where do the responsible-lending obligations sit? #

Conforming to an open protocol on your own surface does not move the regulatory burden, because these protocols are jurisdiction-neutral and carry no obligations of their own. In Australia, credit licensees must comply with the responsible-lending conduct obligations in Chapter 3 of the National Consumer Credit Protection Act 2009, administered by the Australian Securities and Investments Commission (ASIC). In New Zealand, consumer credit is governed by the Credit Contracts and Consumer Finance Act, with regulatory responsibility transferring from the Commerce Commission to the Financial Markets Authority, the markets-conduct regulator, effective 1 July 2026. In both jurisdictions the licensed lender carries the responsible-lending obligation. Implementing an open standard on your own surface keeps those obligations where they already sit, which is the defensible posture.

This is a point about where control and accountability align. NETEVO encodes obligations like these as executable controls in policy-as-code; the application of any specific obligation to any specific factual scenario is for the licensee's regulatory advisers in light of the facts.

Where to read next

The path is editorial to solution to engagement. If being directly reachable by AI agents is the position you want, the solution pages below describe how the surface is built and governed.

AI Agent Infrastructure

The build-side engagement — intent engineering, MCP architecture, multi-agent orchestration, and agent-native product design that make your own surface reachable by AI agents.

View solutionAI Governance & Readiness

The regulatory-readiness sibling — encoding responsible-lending and AU obligations into executable controls and policy-as-code, so the duty stays defensibly on your licence.

View solutionArchitectural AI: Where the Leverage Lives

Why investment in machine-readable product surfaces — the surfaces agents transact against — compounds, while more human-readable content does not.

Read pillarAgentic Procurement Failure

The safety-side companion — what an enterprise must design against when an autonomous agent, not a human at a screen, becomes the consumer of a vendor system.

Read pillarAgent-Ready Lending (depth paper)

The next rung on the ladder — the full treatment of certification chokepoints, the agentic due diligence checklist for an aggregator pilot, and where the responsible-lending duty sits across AU and NZ.

Read the whitepaperAI Traffic Monetisation

The topic pair — the content-owner side of the same shift. Agent-mediated credit and metered content access ride the same payment and identity rails; this insight covers the discoverable-versus-gated decision for AI traffic.

Read insightQuestions

Frequently asked questions

Category, vocabulary, and strategy questions. How a lender builds an agent-reachable surface — MCP endpoints, agent-native product design, policy-as-code governance — is answered on the AI Agent Infrastructure solution page.

Is agent-ready lending the same as listing in an AI marketplace?

No. Listing makes you inventory inside another company's surface. Agent-ready lending makes your own surface the destination an agent reaches directly, so the customer relationship and the regulated journey stay with you rather than with the marketplace operator.

Does conforming to MCP, A2A, or AP2 mean joining one operator's platform?

No. These are open, multi-vendor standards you implement within your own systems. Conforming to the published specification on your own surface is what makes you addressable by agents; it does not require joining any single operator's platform or registry.

Do these protocols change who carries the responsible-lending obligation?

No. They are jurisdiction-neutral and transfer no compliance burden, so the licensed lender holds the obligation, the disclosure, and the audit trail. Implementing an open standard on your own surface keeps those obligations exactly where they already sit.

What is the single most useful question to ask an aggregator?

Who runs the reference implementation, the benchmark, and the registry, and on what commercial terms. An open licence governs the specification document; it says nothing about who operates those three governance functions, which is where the power actually sits.

Is 'certified' a guarantee of neutrality?

No. Certification is only as neutral as the standard and the body behind it. A badge one party can withdraw, tier, or re-cut is leverage, not assurance. Certify against a neutral standard, not against one operator's instance of it.

How does agent-ready lending relate to agentic credit broking protocols (ACBP)?

They address the same shift from two ends. Agentic credit broking protocols are an emerging class of standards for AI agents transacting credit on a consumer's behalf — the first is now published as a public draft — and most position an intermediary at the centre of the journey. Agent-ready lending is the lender's side of the same shift: conform to the open agentic-commerce standards (MCP, A2A, AP2) on your own surface, so an agent can reach you directly while the customer relationship, the audit trail and the licence stay in-house. The standard is neutral. Where you implement it decides who holds the customer.

Should a lender join an agentic credit broking pilot or build its own surface?

It is not either-or, but the order matters. Conforming to the open standard on your own surface preserves your optionality; joining a single operator's pilot as an endpoint does not, because the benchmark, the registry and the audit history accrue on their side. Before joining any pilot, establish who runs the reference implementation, the benchmark and the registry, and on what terms. An open licence on the specification is not the same as a neutral operator behind it.